Zero To One by Peter Thiel — Book Summary and Notes

Every moment in business happens only once. The next Bill Gates will not build an operating system. The next Larry Page or Sergey Brine won't make a search engine

"Every moment in business happens only once. The next Bill Gates will not build an operating system. The next Larry Page or Sergey Brine won't make a search engine... If you are copying these guys, you aren't learning from them."

Technology has stagnated in the present. Much of what most people do builds on ideas of the past. It's easier to copy something than to create something new. This moves the world from 1 to n, refining something familiar. However, making something new moves us from 0 to 1.

In Zero to One, PayPal co-founder Peter Thiel contends that creating new things is the best way to profit economically and the only path to human progress.

The paradox of teaching entrepreneurship is that such a formula cannot exist; because every innovation is new and unique. Successful people find value in the most unexpected places. They do this by thinking about business, not in terms of formulas, but first principles.

Zero To One

Notes on Startups, or How To Build The Future By Peter Thiel with Blake Masters

1. The Challenge of the Future

Thiel likes to ask interviewees what he calls a contrarian question: "What important truth do few people agree with you on?"

A good answer takes the following form: “Most people believe in X, but the truth is the opposite of X.”

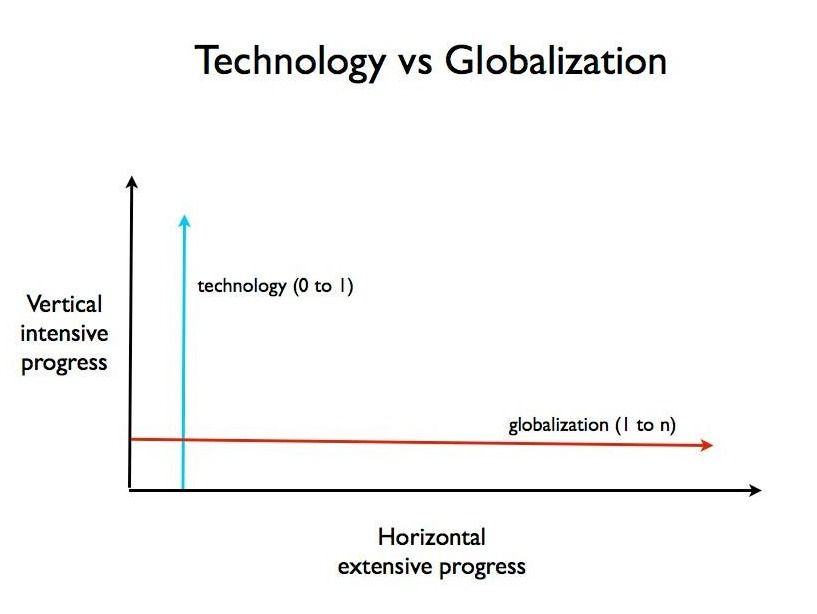

Thiel answers is that most people believe globalisation will determine the world's future, but he thinks it is the technology that will.

The Path of Progress

- Horizontal progress results from duplication success — going from 1 to n.

- It's easy to imagine because we already know what it looks like

- Vertical progress requires doing something new — going from 0 to 1.

- It's more challenging to envision because nobody else has ever done it.

Globalisation is horizontal progress — it takes something that functions in a particular place and expands it everywhere.

Technology is vertical progress — it encompasses something new and better.

Startup Thinking

Startups consisting of a few people with a mission are the source of most technology

- Big organisations tend to avoid risk

- A brilliant loner doesn't have the means to create a new industry

Startups work because it takes multiple people to create new technology, and smallness for momentum and flexibility. Small companies encourage new thinking because they know it is their biggest asset. The first job of a startup is to question everything and rethink business from the beginning.

2. Lessons of the Dot-Com Bubble

Remember the question, "What important truth do few people agree with you on?", try starting with: "What does everyone agree on?"

The absolute truth often is the opposite of what everyone agrees is true. People who are blinded by conventional wisdom can't produce anything new.

Conventional wisdom created the dot-com bubble. The principle that companies need to profit was replaced in the late 1990s by a delusion that became the new conventional wisdom: companies racking up never-ending losses were succeeding because the losses would act as 'investments' for future success.

Thinking clearly about the future requires questioning what everyone "knows" about what happened in the past.

From the dot-com crash, four lessons became regarded as too valuable to be inferred:

- Make incremental Advances: Be wary of big visions that drive bubbles. Move forward with small, measurable steps.

- Stay lean and flexible: Don't be obsessed with planning. Instead, try to experiment, iterate on the things that work, and treat entrepreneurship as "agnostic experimentation".

- Build on the competition: Build your business by improving on recognisable products in demand that other competitors offer.

- Focus on product, not sales: Tech is about product development, not distribution.

However, contrary to common belief, the opposite of each lesson is likely more accurate:

- It's better to be bold than inconsequential.

- An imperfect plan is better than none.

- Don't Compete: competition destroys profits.

- Sales strategy matters as much as the product.

3. Competition and Monopoly

Anyone considering a startup should ask: "What valuable company is nobody building?"

Creating value is not enough—you also need to capture some of the value you create.

Perfection Competition

Every firm in a competitive market is undifferentiated and sells the same products. Since no firm has any market power, it must sell at whatever price the market determines. In perfect competition, no one profits in the long run.

Monopoly

While competing companies must sell their product at the market price, a monopoly owns the market and sets the price.

Companies often lie about their market status so that all businesses seem similar. However, most companies are either closer to one extreme or the other—perfect competition or monopoly.

Monopolies lie because acknowledging their market control attractions unwanted attention and attacks. They downplay their status by exaggerating the power of their nonexistent competition.

Non-monopoly companies say the opposite, claiming to be in a league of their own. They downplay their competition by defining their market as so narrow that they stand out. They describe their market as the intersection of various smaller markets.

Monopoly Characteristics

1. Proprietary Technology

Proprietary technology makes your product almost impossible to replicate. For prior technology to give a monopolistic edge, it needs to be at least 10 times better than the next best alternative.

- Create something new

- Improve Functionality so dramatically that it eliminates competition

- Improve Design so dramatically that it eliminates competition

e.g. Paypal improved buying and selling on eBay exponentially by enabling the immediate transfer of funds

2. Network Effects

Network effects make a product more valuable as more people use it, providing an immediate valuable to its earliest adopters which allow for growth.

e.g. The more your friends use Facebook, the more value you get from being on the platform.

3. Economics of Scale

A monopoly gets stronger as it grows because the fixed costs of creating a new product are spread over a greater volume of sales, so the price per unit declines. A good startup has the potential for scale built into its first design.

e.g. Twitter can increase the number of users without adding more features

4. Branding

Creating an unassailable brand is integral to having a monopoly.

e.g. Apple

4. Success Comes from Planning

Its possible luck could play a role in individual success, but chance is not sufficient to explain how people can achieve sustainable success.

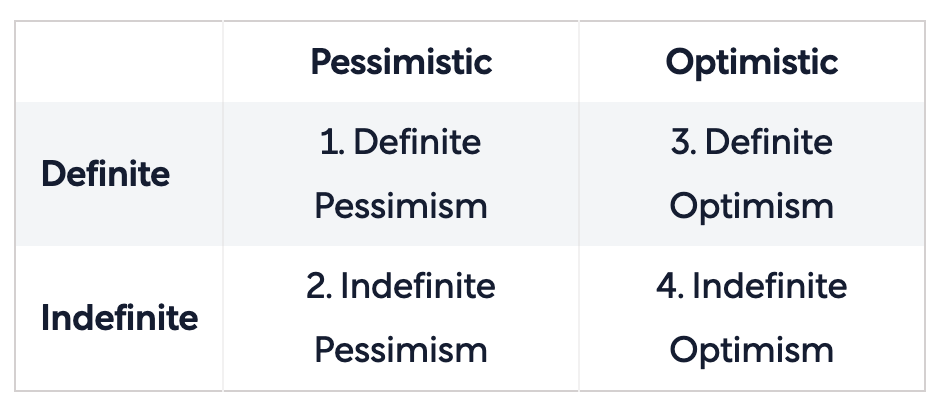

Today, whether you think of the future as determined by chance or design affects how you act in the present and whether you ultimately succeed.

Ways of Thinking about the Future

Your belief about the future determines what you do in the present. People think of the future as either:

- Definable and Definite

- A Hazy Uncertainty

In middle school, students start collecting "extracurricular activities. In high school, students compete to excel in everything. By the time they reach college, students have assembled a widely diverse resume to prepare for a seemingly unknown future; they're ready for everything and nothing.

Rather than working to be well-rounded and indistinguishable from anyone else, a student who sees the future as definable focuses on devoting their time and effort to specifics.

- Definite Pessimism: A definite pessimist believes the future is bleak and, therefore, tries to prepare for it.

- Indefinite Pessimism: An indefinite pessimist expects a grim future, but he does not plan to do anything. They expect decline and wait for it to come to them.

- Definite Optimism: The definite optimist believes the future will be better due planning and effort. Scientists, investors, and entrepreneurs with this outlook made the world richer.

- Indefinite Optimism: An indefinite optimist believes the future will be better but attributes this to chance rather than effort or planning. Instead of building new things, indefinite optimists rearrange existing things.

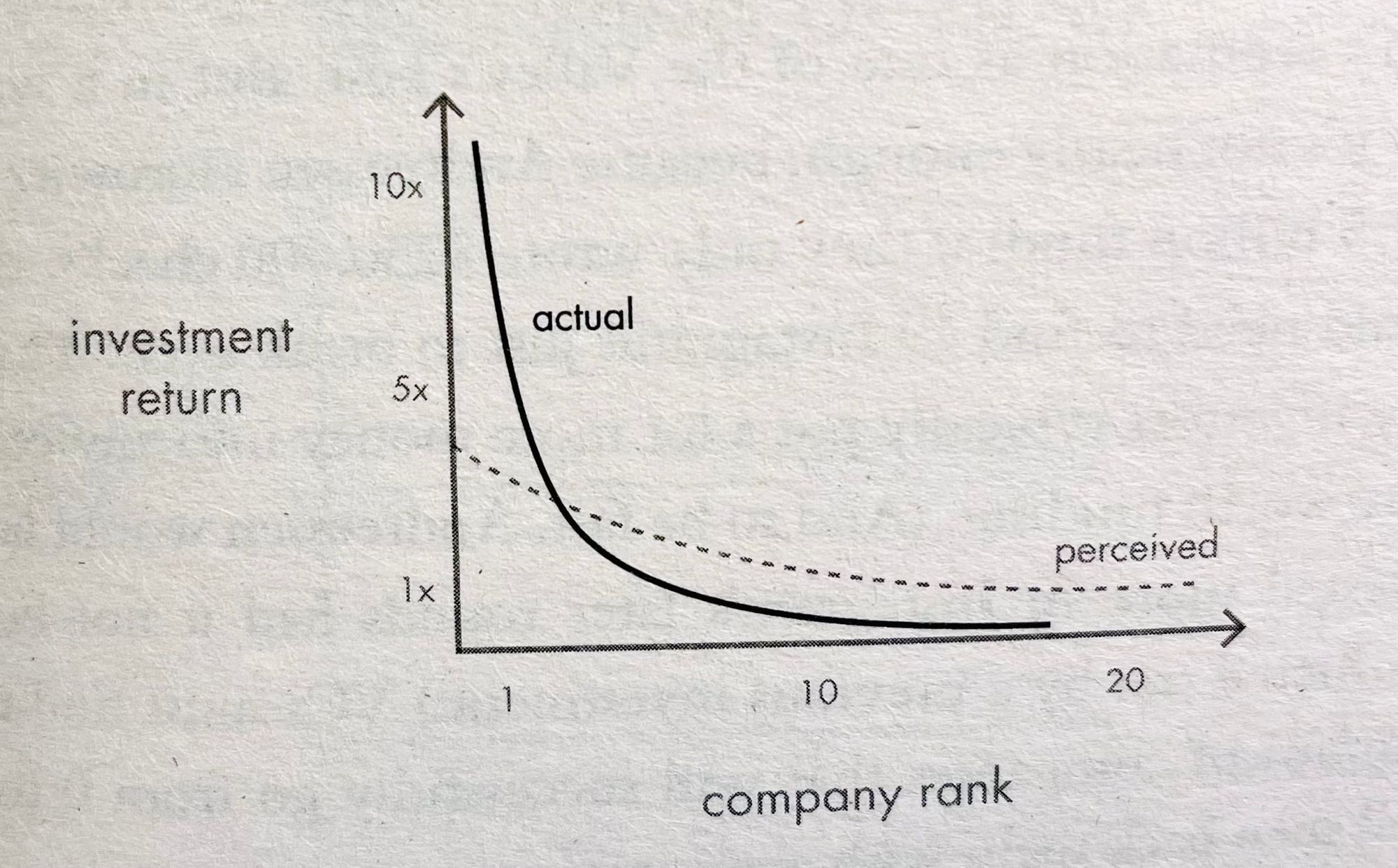

5. The Power Law

The power law describes a common phenomenon in which small changes have disproportionate results. It is key to understanding how startups achieve exponential success.

- One market will bring the greatest success

- One distribution strategy will outperform all others

- Some moments will count more than others

- What's more important probably is not obvious

6. The Value of Secrets

Creating a business that no one else can compete with starts with discovering and building on a secret—it can be an untapped opportunity for a different way of looking at a problem

Most people in the present as if there's nothing left to be discovered; they accept conventional wisdom.

Four trends have undermined our belief in secrets

- Incrementalism: Formal educations teaches people things by taking one small step at a time. Students rarely get credit for thinking outside the box or learning something not on the test. However, if they followed instructions, they'll get an A.

- Risk Aversion: People are afraid to look for secrets because they fear being wrong.

- Complacency: Social elites have the most freedom and ability to explore new thinking, but they come to like their comfortable position and don't want to rock the boat

- Homogenisation: As globalisation increases, people increasingly view the world as a single market where everyone competes equally. They believe if there were anything new to discover, someone in the global talent pool would have already done it.

Finding Secrets

The best place to find secrets is to ask questions no one is asking and look where no one else is looking.

The best entrepreneurs know this: every successful business is built around a secret hidden from the outside. A great company is a conspiracy to change the world; when you share your secret, the recipient becomes a fellow conspirator.

7. Building a Strong Foundation

While all startups are different, every startup needs to get certain things right at the start because it's impossible to fix them later.

The First and Most Crucial Decision You Make is Whom

While all startups are different, every startup needs to get certain things right at the start because it's impossible to fix them later.

Ownership, Possession, and Control

- Ownership: Who will own the company's equity (founders, employees, investors)

- Possession: Who will run the company day-to-day (founder, CEO, manager)

- Control: Who will govern the company (A board of directors)The potential for conflict increases over time as interests diverge. In the boardroom, less is more. The smaller the board, the easier it is for the directors to communicate, reach consensus, and exercise effective oversight—every single member of the board matters. A board of three to five members is the ideal size.

Compensation

A CEO of a venture-funded startup should not be paid more than $150,000 a year.

High pay encourages the CEO to protect their salary and minimise problems rather than exposing and fixing them

- It enables the executive to focus on increasing the value of the company.

- It motivates employees to work harder.

Vested Interests

Equity is the one form of compensation that can effectively orient people toward creating value in the future. However, giving everyone equal shares is usually a mistake: everyone has different talents, responsibilities, and opportunity costs.

Anyone who prefers owning a part of your company reveals a preference for the long-term and a commitment to increasing your company's value.

8. Building a Cohesive Team

No company has a culture; every company is a culture. A startup is a team of people on a mission.

Recruiting

Talented people don't need to work for you; they have plenty of options. You must be able to articulate to the 20th candidate why he should join your company.

- Your Mission: Explain what makes your mission unique and compelling. What are you doing that no one else is doing?

- Your Team: Show potential employees that the people on your team are the kind of people they want to work with.

Most conflicts in a company stem from colleagues competing for the same responsibilities. While creating a team of like-minded people, you should avoid having this kind of competition by making each person responsible for doing one specific thing. Each employee should know managers would only evaluate them on that responsibility.

9. If You Build it, You Still Have to Sell It

- Customer Lifetime Value (CLV): The total net profit that you earn on average throughout your relationship with a customer

- Customer Acquisition Cost (CAC): The amount you spend to get a customer.

Complex Sales

- The only way to sell some of the most valuable products ($1 mil to $100 mil)

Personal Sales

- $10,000 to $100,000

- The challenge is establishing a process in which the sales team can move the product to a broader audience.

Marketing and Advertising

- Effective for selling low-priced products for mass consumption

- Every entrepreneur envies a recognisable ad campaign, but startups should resist the temptation to compete with more prominent companies in the endless content on the most elaborate PR stunts.

Viral Marketing

- The cheapest and fastest way to sell a product is to encouraging existing users to invite additional users.

- Extremely short cycle timesd

10. Making Green Tech Work

Questions to Ask

- Engineering: Is your technology a significant advice or only an incremental improvement?

- Timing: Is this the right time to sell this technology?

- Monopoly: Are you targeting a big share of a small market?

- People: Do you have the right people on your team?

- Distribution: Do you have a plan to sell your product?

- Durability: Will you dominate your market in the next 10 to 20 years?

- Secret: Have you identified a unique opportunity overlooked by everyone else?

In A Nutshell: Zero To One

Our task today is to discover distinctive ways to create new things that will make the future different and better—to go from 0 to 1. Only by seeing our world as fresh and strange as it was to our ancestors can we both re-create it and preserve it for the future.